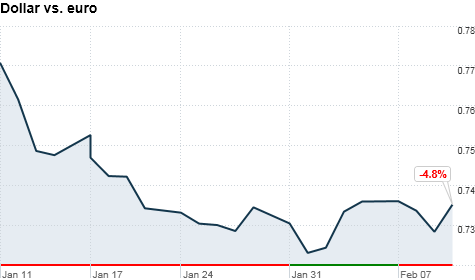

European peripheral debt concerns are back front and center, with Portuguese bond yields hitting new euro-era all-time highs and CDS rising again. Yet there doesn’t seem to be any single development behind the renewed tensions. If we were to suggest the primary cause, it would be our view of a slow-developing sense of disappointment over EU negotiations on strengthening the EFSF (the current stabilization fund for peripheral bailouts, to be replaced by the so-called permanent crisis resolution, the ESM-European Stabilization Mechanism in 2013).

Bond markets have essentially demanded an expanded EFSF to minimize the risk of a sovereign default over the next two years, judging the current plan too small in the event of Portugal and Spain needing bailouts. Germany has rejected both expanding the size of the fund and allowing it to purchase peripheral government debt in the secondary market, two key elements markets were counting on. Italy is protesting any mandated annual debt reduction targets, undermining the very credibility of the “Competitiveness Package,” which is intended to convince markets European countries can get their debt under control. Lacking these critical pieces, it appears to us that markets are preparing to be underwhelmed by the final program. While negotiations may still produce a more credible reinforcement of the EFSF, markets seem to be pricing in disappointment and renewed fears of inevitable debt restructuring.

Eurozone finance ministers are holding a regularly scheduled meeting early next week and we will be alert for shifts in bargaining positions. But between the renewed strength in the USD (see below) and increasing doubts on the European debt plans, EUR/USD appears set to move lower again. Key support below is found between 1.3450/3500, the prior range highs in Dec.-Jan, and a break below there would target weakness to the 1.3360/65 daily Kijun line initially, and then the 1.3185 cloud base. Attempts to break above 1.3750/3800 have failed repeatedly, so continuing to sell strength is our preference.

All eyes on Mervyn King

The governor of the Bank of England Mervyn King gets to face his critics on Thursday when he presents the first Inflation Report of 2011 on Thursday. It t will go some way to telling us how close the Bank is to a rate in an environment where it is being increasingly criticised for leaving rates low while inflation pressures mount.

At the last Report in November the Bank’s forecast for the trajectory of prices was considered dovish. It predicted inflation remaining about 3.5 per cent for the first half of this year before falling rapidly to below the Bank’s 2 per cent target throughout 2012. This justified King’s view that monetary policy needs to remain loose to ward off the spectre of deflation.

Analysts will want to determine if these forecasts have changed based on the continued price pressures in the UK economy. UK price data is released on Tuesday and it is expected to rise to 4 per cent, 2 per cent above the target, due to rising commodity prices and the increase in sales tax that came into effect at the start of the year. Essentially, if the Bank sees inflation remaining elevated for longer than the second half of 2011, markets will perceive this as hawkish, which could boost the pound. It would also increase speculation of a near-term rate hike possibly as early as March due to the historical tendency of the Bank to move on rates the month after an Inflation Report. However, if there has not been a change to the forecasts then the markets will rapidly start to re-assess the 90 basis points of hikes priced in for the next 12 months. This would likely drag the pound lower.

There is no denying that price pressures have picked up in recent weeks and months, producer prices continued to rise in January, which will probably weigh on CPI on Tuesday. However, part of this is due to the rise in the sales tax, and hiking rates on the back of an increase in taxes could be too much for the fragile UK economic recovery to take. So this Inflation Report isn’t necessarily the game-changer that some may think it is. The growth outlook is still uncertain: economic statistics have been all over the place and austerity cuts have yet to take hold in a major way, which makes hiking rates in the current environment as risky as leaving them low even though fears are growing that inflation will become entrenched in the UK economy.

Overall, it’s likely to be a volatile few weeks for the pound. Above 1.6000 GBPUSD is in a technical uptrend, however, gains above 1.6250 have been fleeting and investors have been unwilling to establish pound longs above here, for good reason in our opinion. Below 1.5880 the rhythm of the pound has changed, and we could see GBPUSD start to turn lower.

The outlook for USD/JPY looks promising

Over the past few months we have frequently noted USD/JPY’s divergence from US Treasury yields in contrast to the historically positive correlation. While the rationale for higher rates in the US is clearly debatable, we believe it is predominantly due to a strengthening US economic outlook, since the timing of most yield advances was on the back of better than expected US data, rather than credit concerns over federal and state deficits. While the yield curve has shifted markedly higher since the 4th quarter, the sharper ascent over the past few weeks finally sparked currency traders to take action in line with historical relationships (higher US rates, higher USD/JPY). Over the past week USD/JPY has broken above the recent consolidation pattern (connecting the December and January highs) as well as above the 55 and 100-day SMA’s.

On Monday, Japan is expected to report their 4Q preliminary GDP – consensus is looking for -2.0% annualized vs. +4.5% last quarter. Although a negative print is widely anticipated, it could further underpin Japan’s slowing and highlight their own massive deficit and debt overhang, which should ultimately undermine the Yen longer-term. Of late we have seen a lack of enthusiasm by Japanese investors to firmly remain in their Yen long positions, conceivably affirming the negative outlook. In addition, seasonal patterns point to further strength for USD/JPY over the next few weeks and we also believe Japanese year end repatriation flows, towards the end of March, are likely to be smaller than in years past. Furthermore, our proprietary interest rate and equity models suggest fair value for USD/JPY is around 89-92, which is still approximately 600-900 pips from where it’s currently trading. In the shorter-term, the dollar needs to break above 83.70 (January 7th high) and 84.40/50 (series of December highs) before a more significant advance can take hold.

RBA expectations driving the Aussie

On Tuesday, the Reserve Bank of Australia will release its Monetary Policy meeting minutes detailing the Jan. 31 meeting. Recent reports from the RBA, as seen in last week’s quarterly Monetary Policy Statement and RBA Governor Glenn Stevens’ speech before a Parliamentary economics committee on Friday, indicate that while long term growth is expected to be robust, the near term economic outlook has been negatively impacted by adverse weather conditions (Q1 GDP could be 1% lower than pre-flood forecast) and is likely to warrant the bank to stay on hold for some time.

Governor Stevens stated that it is “probably reasonable that no hike (be made) for some time”. While he noted that the RBA believes that the CPI is likely to rise to 3% (the upper end of the RBA’s target range) in Q2 2011 instead of the previously forecast 2.5%, this figure showed “inflation a little lower than we had thought”. The tone of the RBA governor was much less hawkish than last week’s Monetary Policy Statement and sent the Aussie dipping below parity against the U.S. dollar. Stevens also noted that China is currently stronger than expected and that “China demand for resources to last some time”. As China has been tightening and is expected to continue this policy, there is potential risk for a slowdown in China which may shift expectations in Australia to the downside and weigh on AUD. The week ahead will see China PPI, CPI and trade balance data for January to provide more insight into the Chinese economy. The upside risk is for higher than expected inflation in Australia which may prompt the RBA to take a more hawkish stance. Such a scenario would result in a stronger AUD.

Short term weakness in AUD/USD can be viewed as buying opportunities as the longer term outlook remains bullish. Key technical levels include the daily Kijun line and 21-day sma which currently converge around 1.0000/10. The base of the daily ichimoku cloud, 21-week sma and 100-day sma currently comes in around 0.9900/10 as the next significant support zone. Key levels to the upside are the 1.01 pivot and the 1.02 figure ahead of post-float highs which are around 1.0255/60.

Technicals suggest a short term bottom for the buck

Safe haven and capital inflows saw the buck gain further traction this week. Uncertainty in Egypt alongside a substantial shift in capital flows from emerging market to developed economies have translated into weekly gains of about +0.5% for the USD Index. The reversal in the buck’s fortunes have led to technical developments that suggest a continuation for the current USD uptrend – the USD Index may have completed an inverted H&S bottom with a measured move objective slightly short of the key 80.00 level. The technical pattern formation in the USD Index has been corroborated by EUR/USD – the single currency has broken below H&S neckline support around the 1.3550 level suggesting a measured move objective towards the 1.3300 figure. Additional evidence for further dollar strength can be seen in the USD Index ascent above the daily Ichimoku cloud base – a daily close above 78.55 would be needed for technical upside confirmation. The move above significant Ichimoku levels has also been reflected in USD/JPY. The pair has firmly traded above daily cloud tops (82.50) and looks set to close above the weekly Kijun line (83.25). Recent price developments could be the beginning of a 2011 greenback revival as confirming signals are developing from both western and eastern methods of technical analysis.

Key data and events to watch in the week ahead

United States: Monday – Fed’s Dudley speaks at regional economic briefing Tuesday – Feb. Empire Manufacturing, Jan. Import Price Index, Jan. Advance Retail Sales, Dec. TIC Flows, Dec. Business Inventories, Feb. NAHB Housing Market Index Wednesday – Feb. 11 MBA Mortgage Applications, Jan. Housing Starts, Jan. Building Permits, Jan. PPI, Jan. Industrial Production, Jan. Capacity Utilization, FOMC Meeting Minutes Thursday- Jan. CPI, Weekly Jobless Claims, Jan. Leading Indicators, Feb. Philly Fed, Bernanke testifies on Dodd-Frank Friday – Bernanke speaks on global imbalances in Paris.

Eurozone: Monday – Dec. Industrial Production, EU finance ministers meeting in Brussels Tuesday – 4Q A GDP, Feb. ZEW Survey of Economic Sentiment, Dec. Trade Balance, German 4Q Prelim. GDP, German ZEW Surveys Thursday – Feb. Adv. Consumer Confidence Friday – Jan. Producer Prices.

United Kingdom: Tuesday – Dec. DCLG UK House Prices, Jan. CPI, Jan. Retail Price Index, Jan. RPI Wednesday – Jan. Claimant Count Change, Jan. Jobless Claims Change, Dec. ILO Unemployment Rate, Bank of England Inflation Report Friday – Jan. Retail Sales

Japan: Sunday – 4Q Prelim. GDP Monday – Dec. F. Industrial Production, Dec. F. Capacity Utilization Tuesday – BOJ Target Rate, Jan. F. Machine Tool Orders, Dec. Tertiary Industry Index

Canada: Wednesday – Jan. Leading Indicators, Dec. International Securities Transactions, Dec. Manufacturing Sales Thursday – Dec. Wholesale Sales Friday – Jan. Consumer Price Index, Jan. BoC CPI Core

Australia & New Zealand: Sunday – Australia Dec. Home Loans, NZ 4Q Retail Sales Monday – Australia Reserve Bank’s Board February Minutes Tuesday – Australia Dec. Westpac Leading Index, Australia Feb. DEWR Skilled Vacancies, Jan. New Motor Vehicle Sales Wednesday – RBA’s Lowe gives speech on 2011 Economics in Sydney, NZ Jan. Business PMI, NZ 4Q Producer Prices Inputs & Outputs, NZ Finance Minister English Speaks

China: Feb. 10-15 – Money Supply (M2) Sunday – Jan. Trade Balance, Jan. Exports & Imports, Monday – Jan. Producer Price Index Thursday – Conference Board China December Leading Economic Index.